MET Magazine Special Report

Two wars, one in Eastern Europe and one now consuming the Middle East, are reshaping the cost structure and supply chains of the global pulp, tissue, and nonwovens industry. What follows is an assessment of where things stand — and where the uncertainty remains.

There is a version of this story that writes itself. Two wars. Shipping routes in chaos. Oil above a hundred dollars. Energy bills that never fully came back down. For the pulp and paper industry, the headline practically assembles on its own.

But the reality, as anyone working in procurement or production planning will tell you, is messier than the headlines suggest. Not every company has been hurt in the same way. Not every market has moved in the direction you might expect. And some of the most consequential effects — the slow structural ones, the ones that don’t make the news — started well before the first shot was fired.

EUROPE’S ENERGY WOUND — STILL OPEN

Before we get to oil tankers and drone strikes, it is worth revisiting what the Russian invasion of Ukraine did to European energy markets — because that wound has not fully healed, and it forms the backdrop against which everything that followed has played out.

When Russian gas supplies to Europe began falling sharply in 2022, wholesale gas prices in Europe spiked to levels more than ten times those of early 2021. For paper mills, which depend heavily on thermal energy for drying and chemical processes, the consequences were immediate. Energy can represent 20 to 30 percent of a mill’s total production costs in normal times. In 2022, for some facilities, it became the dominant cost line altogether.

Russia’s share of EU pipeline gas imports fell from roughly 40 percent in 2021 to around 6 percent by 2025. Europe adapted through LNG imports, demand reduction, and a partial shift to renewables, but adaptation is not the same as recovery. Household and industrial gas prices across much of the EU remained substantially above their pre-war levels into 2026. For mills in Poland, the Baltic states, and parts of Central Europe, the increase has been particularly sharp and persistent.

Metsä Board offers a sharper picture of how the pressure has accumulated. The Finnish paperboard producer’s 2025 results swung to a comparable operating loss of EUR 80 million, from a EUR 69 million profit the year before, as sales value fell 8.4 percent under the combined weight of US import tariffs hitting its Husum mill and weak European paperboard demand. The board proposed no dividend for 2025. Q1 2026 brought modest improvement, comparable EBITDA of EUR 17 million, helped by the company’s transformation program delivering EUR 100 million of run- rate EBITDA improvement by quarter-end, but the underlying environment remained difficult. The pressure showed up across the wider Metsä group: at sister company Metsä Tissue, change negotiations were concluded in March 2026 with a reduction of 50 jobs, and at Metsä Fibre, the Joutseno pulp mill was placed on indefinite shutdown at the end of Q1 2026. Metsä Board’s own Q1 2026 interim report named the geopolitical channel directly: ‘The increase in oil and natural gas prices resulting from the conflict involving Iran is creating upward pressure on logistics and chemical costs. Metsä Board’s high energy self-sufficiency supports its competitiveness.’ That is one of the cleaner statements of the producer-side trade-off the article has been tracing — exposed to the same input shocks as the rest of the industry, but better positioned to absorb them.

The Russian conflict also redirected pulp supply flows in ways that have not fully resolved; Russia had been a meaningful supplier of softwood kraft pulp and paperboard to European buyers; sanctions and trade restrictions pushed those volumes toward Asia instead. As a result, European mills that had relied on competitively priced Russian fiber had to find alternatives, mainly from Scandinavia, Canada, and Brazil, at higher cost and with longer lead times.

The sector-wide numbers, published by CEPI in early 2026, put the cumulative damage in context. European paper and board production declined a further 1.5 percent in 2025, with graphic paper down 7.2 percent. Tissue slipped 0.8 percent. CEPI cited high energy and manufacturing costs relative to global competitors, alongside geopolitical challenges and rising trade tensions, as the principal drivers. Across packaging, tissue and specialty paper combined, production remains 6.8 percent below the record level registered in 2021 — a gap that has proved stubbornly resistant to recovery.

.jpg)

THE RED SEA: WHEN THE SHORTEST ROUTE BECAME THE RISKIEST

Late 2023 brought a different kind of disruption. Attacks on commercial vessels in the Red Sea triggered a sharp deterioration in maritime security along one of the world’s most critical shipping corridors. Major container lines began rerouting ships around the Cape of Good Hope, a detour that adds roughly 6,000 nautical miles and anywhere from ten days to two weeks to a typical Asia–Europe voyage.

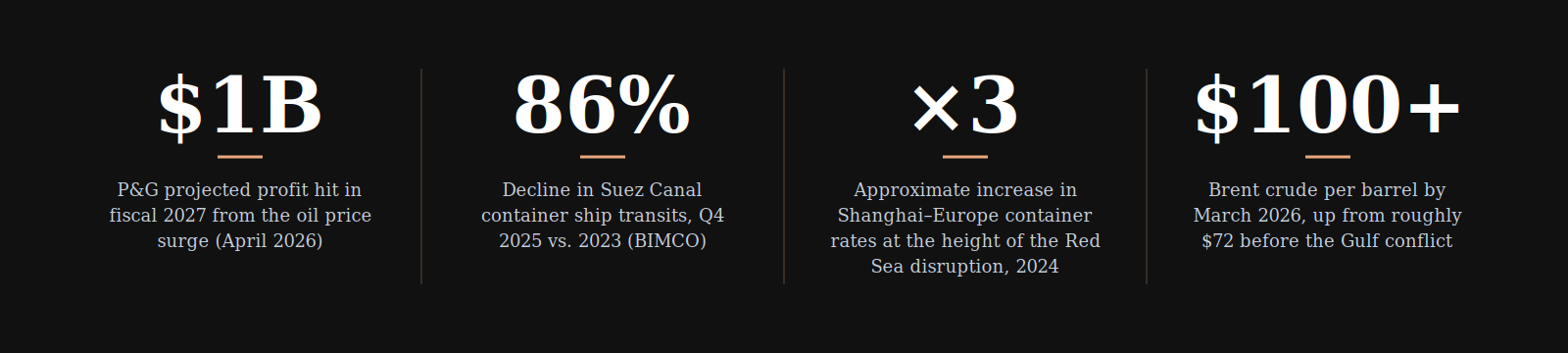

The Suez Canal normally handles more than 80 percent of container traffic between Asia and Europe. By the first half of 2024, vessel transits through the canal had fallen by a similar magnitude year-on-year, according to vessel tracking data. As ships spent longer at sea, effective global container capacity tightened and freight rates adjusted upward accordingly. At the peak, Shanghai–Europe rates roughly tripled compared to late 2023 levels. At the peak, Shanghai– Europe rates roughly tripled compared to late 2023 levels.

The shift proved durable. According to BIMCO, Suez transits in the fourth quarter of 2025 were still 86 percent below 2023 levels. By early 2026, total canal traffic remained around 60 percent below pre-crisis levels, meaning the Cape of Good Hope rerouting had moved beyond a temporary adjustment and become the default operating pattern for Asia–Europe container shipping.

.jpg)

For pulp exporters, shipments from a Northern Europe to China suddenly took two weeks longer and cost materially more to ship. Some supply models suggested that sustained delays in European pulp deliveries could tighten the supply– demand balance in China and push prices higher, though the margin for error in such forecasts remains considerable.

The tissue segment has its own particular vulnerability here. Pulp is the dominant input cost in tissue manufacturing, it can account for as much as 70 percent of parent roll production expenses. When pulp prices move, tissue margins move with them, usually on a lag. Companies running just-in- time inventory models found themselves scrambling for buffer stock. Those with longer-term supply contracts were better insulated, at least initially.

By mid-2025, freight rates had pulled back from their peak as shippers adjusted lead times and ordered further in advance. That kind of adjustment tends to get mistaken for stability. In late February 2026, the Gulf conflict arrived to correct that impression. By the week ending 26 March 2026, Drewry’s World Container Index had risen for four consecutive weeks to $2,279 per 40-foot container, with Asia–Europe lanes leading the gains — Shanghai–Genoa up 12 percent to $3,474, Shanghai–Rotterdam up 3 percent. Drewry attributed the move directly to Middle East tensions and Strait of Hormuz disruptions tightening bunker fuel availability, with carriers responding through emergency fuel surcharges and slow steaming. By late April 2026, rates had eased again under pressure from weak seasonal demand and excess fleet capacity, but the Suez Canal remained far from a return to normal, and routing decisions that would once have been automatic had become, for many carriers, a calculation made week by week.

THE GULF CONFLICT: AN OIL SHOCK ON TOP OF EVERYTHING ELSE

.jpg)

Brent crude was trading around $72 per barrel when the Gulf conflict began in late February 2026. Within four weeks it had crossed $100, one of the sharpest single-month moves on record, as fighting spread and the Strait of Hormuz — through which around 25 percent of global seaborne oil trade flows — came under threat. The peak, briefly, was higher still. That kind of move, sustained rather than reversed, changes the arithmetic for every energy-intensive manufacturer on the planet. Where the Russia–Ukraine war had been a slow burn on European energy costs, this was an acute supply rupture.

For the paper and nonwovens industries, the Gulf conflict is functioning less like a traditional commodity spike and more like a system-wide inflationary shock. Oil prices feed simultaneously into energy markets, petrochemical feedstocks, transportation costs, packaging materials, and global freight rates. Mills dependent on LNG face rising power and thermal energy costs just as nonwovens producers absorb higher polypropylene and polyester pricing. At the same time, disrupted shipping routes and elevated bunker fuel costs raise the price of moving pulp, chemicals, finished products, and spare parts through already strained supply chains. The result is a form of synchronized cost escalation across the value chain, compressing margins even where demand itself remains relatively stable.

Damaged LNG infrastructure in Qatar introduced a longer- term complication. QatarEnergy CEO Saad al-Kaabi confirmed that attacks on the Ras Laffan complex, which processes around 20 percent of global LNG supply, had knocked out 17 percent of Qatar’s LNG export capacity, sidelining 12.8 million tonnes of annual production for three to five years. Force majeure was declared on long-term contracts with buyers in Italy, Belgium, South Korea, and China. European buyers who had spent three years diversifying away from Russian gas found themselves facing a new tightening in the very markets they had turned to as an alternative.

Procter & Gamble was among the first major consumer goods companies to put numbers to the exposure, flagging a $150 million after-tax headwind concentrated in Q4 fiscal 2026, and projecting a roughly $1 billion hit to full-year 2027 profit. “A lot of our materials are petrol-based,” CFO André Schulten stated, “so with oil at around $100, there’s a significant impact in terms of input cost.” The specifics cited were plastics and paper for packaging, alongside transportation.

P&G is not a pulp producer, but its tissue and hygiene categories sit squarely in the same cost environment as companies that are. The company has been simultaneously running a broad supply chain restructuring under its Supply Chain 3.0 initiative— an automation and sourcing diversification program that targets $1.5 billion in gross savings, and is now being used as a live operational response to the Gulf conflict, absorbing force majeure disruptions from upstream suppliers while protecting brand investment and service levels downstream.

The Q1 2026 results from Essity provide one of the clearest views on what geopolitical cost pressure looks like inside a tissue producer’s income statement. At group level, sales grew organically, and the EBITA margin expanded 0.4 percentage points year-on-year to 13.9 percent — but the picture inside the segments was less uniform. Consumer Tissue, Essity’s most pulp-intensive segment, reported organic sales down 3.5 percent and EBITA down 11 percent. Personal Care and Professional Hygiene grew. Essity’s own risk disclosure is equally explicit: ‘Ongoing geopolitical tensions, such as the war in Iran and the conflicts in and around the Persian Gulf, contribute to increased economic uncertainty and rising commodity prices.’

Kimberly-Clark’s situation is worth looking at separately. The company had already flagged a $300 million gross tariff headwind in its Q1 2025 results, driven primarily by US-China trade policy rather than the conflicts directly. By Q1 2026, the Gulf conflict had been added explicitly to the company’s list of risk factors, with management citing ‘regional instabilities and hostilities including the war in Iran’ in its forward-looking disclosures. Yet the headline numbers held up: Q1 2026 net sales reached $4.2 billion, up 2.7 percent, though adjusted gross margin compressed 60 basis points to 37.9 percent and CEO Mike Hsu CEO Mike Hsu noted the company had built share momentum “despite continued geopolitical and macroeconomic uncertainty”. The company is also in the middle of significant structural change, divesting its International Family Care and Professional business as part of a broader reshaping of the tissue and hygiene sector’s downstream operations.

Whether the combined picture — tariff headwinds, conflict-linked input pressure, and structural reshuffling — meaningfully insulates a global tissue business from sustained energy and fiber market volatility is something the industry will be watching closely over the next few years.

NONWOVENS: THE PETROLEUM PROBLEM

The nonwovens industry occupies a particular position in this story because its exposure to petroleum is direct rather than indirect. Paper mills buy energy and pulp; nonwoven producers buy polypropylene and polyester — materials whose prices are set in petrochemical markets that track crude oil closely. Those upstream markets moved sharply in March 2026: European spot polypropylene rose €220 per tonne in three weeks to €1,200 per tonne, Asian polypropylene injection grade jumped $330 per tonne, and S&P Global’s Platts unit recorded the biggest week-on- week price increase in North African polypropylene since its assessment series began in 2021. With Strait of Hormuz transit, in S&P Global’s words, ‘essentially stopped,’ Middle Eastern producers, historically the dominant supplier into European, African, and Turkish markets, withdrew offers within days.

.jpg)

The mechanism ran one step further upstream, through naphtha — the crude-oil distillate that feeds Asia's steam crackers. With Middle East deliveries to Asia down roughly 85 percent in March and benchmark cargoes near $1,300 per tonne, South Korean crackers cut runs and several Asian producers declared force majeure — pushing polypropylene prices up in turn.

The oil shock does not hit all raw material categories equally. Ontex’s Q1 2026 results show this dynamic in concrete terms: index-linked prices for fluff pulp, superabsorbent polymers, and base nonwoven materials actually fell in the quarter, while petroleum-derived backsheets, packaging materials, and transportation costs rose, producing a net cost headwind of €5 million that partially offset the company’s efficiency savings. The Belgian hygiene group, which posted quarterly revenue of €426 million across its baby care, feminine care and adult incontinence portfolio, saw adjusted EBITDA fall 24 percent year on year to €39 million, with the margin contracting to 9.1 percent. Ontex responded with pricing actions and transportation surcharges to partially recover the cost increase, and maintained its full-year outlook, but conditioned it explicitly on ‘gradual easing of the energy crisis,’ a phrase that appeared three times in its April 2026 results statement. That kind of conditional language, from a listed company writing to its regulators, tells you something about how uncertain the cost outlook remains.

That uncertainty makes forward planning genuinely difficult, especially for smaller producers without the purchasing scale or hedging capacity of the industry’s larger players. When the Gulf conflict pushed oil above $100 in early 2026, raw material costs for polypropylene, polyester, viscose fibers, and superabsorbent polymers used in nonwovens had increased between 4 and 11 percent across US and European markets compared with February levels, according to Fastmarkets’ April price assessments. The transmission from oil market shock to contracted fiber prices is slower than spot movements suggest, but the direction of movement was clearly upward.

The industry’s forward projections tell a mixed story. European nonwovens production fell by around 2.2 percent in 2025, according to EDANA, with the hygiene industry— still the largest end-use by volume — down 2.7 percent, and building and roofing materials off by 6.8 percent. Spunmelt, the dominant production process for hygiene and medical applications, declined by 3.3 percent, a figure that tracks closely with the cost pressure on polypropylene. Personal care wipes edged up 0.9 percent, a reminder that demand within nonwovens is not uniform and that some end-uses are more insulated than others. The INDA/EDANA joint outlook through 2028 points to steady global demand growth, led by Asia, but the European picture in 2025 moved in a different direction. Geopolitical cost pressures were not the only factor, competition from abroad and softer demand in key segments also played a role.

INDA, issued a formal statement describing an escalating energy crisis triggered by ongoing global conflicts. The association warned that many member companies were already facing significant increases in operating expenses, and that small and medium-sized producers are the most exposed, lacking the scale to absorb input cost increases that larger integrated companies can partially offset through hedging or long-term supply contracts.

Corporate responses have varied. Magnera — formed in November 2024 through the merger of Berry Global’s Health, Hygiene and Specialties nonwovens business with Glatfelter, creating the world’s largest nonwovens producer — launched “Project CORE” in late 2025, idling approximately 5 percent of global capacity primarily in response to weak hygiene demand in Latin America. In its Q2 fiscal 2026 results, Magnera posted net sales of $796 million, adjusted EBITDA of $90 million, and free cash flow of $73 million, paying down $36 million of debt during the period. The framing had sharpened: CEO Curt Begle told investors that ‘the war in the Middle East has created global challenges on many fronts, including having a direct impact on our raw material and supply chain costs,’ and the company began moving many customers onto monthly pass- through pricing — a deliberate departure from longer-cycle contracts designed to reduce inflation recovery lags.

In Japan, Unicharm — one of Asia's largest hygiene producers — struck a more cautious note: president Takahisa Takahara said inventories were sufficient in the near term, but warned that a conflict persisting beyond the summer would materially affect production costs across its diaper, sanitary and mask lines.

Other producers have held capacity steady or continued long-planned expansions, signaling that the industry has not arrived at a coordinated view of where structural demand and cost pressure will settle.

PULP: NOT ALL PRODUCERS ARE LOSING

Not all producers have been on the losing side of these disruptions. For some producers, particularly those in Brazil, the period has actually been one of record volumes and revenue, even if margins have been more complicated.

Suzano, the world’s largest eucalyptus pulp producer, reported record net revenue of BRL 50 billion for full-year 2025, a 15 percent volume increase driven by its new Ribas do Rio Pardo mill. CEO Beto Abreu noted that pulp prices ‘traded below historic averages’ for much of the year. By Q1 2026, the picture had begun shifting. Pulp prices were recovering in Western markets, with two rounds of price increases totaling $100 per tonne announced for Q1 and Q2 2026. Demand in Europe and North America had exceeded Suzano’s own forecasts, partly driven by paper producers building inventory ahead of anticipated further disruption. The company stated that the Gulf conflict has so far ‘resulted in different dynamics in different markets’ — a headwind in some regions, an unexpected tailwind in others.

Suzano’s oil exposure remains significant: with Brent crude at $104 per barrel as of March 31, 2026, every dollar- per-barrel move translates to BRL 47.1 million in EBITDA impact. Suzano has hedged nearly 90 percent of its 2026 oil-related exposure at average hedge prices of $57 to $69 per barrel, and at current prices expects to receive BRL 810 million in positive cash adjustments from its hedge portfolio over the next two years. Suzano also operates under long-term vessel contracts covering more than 50 vessels, including 10 fully dedicated to its operations, a logistics structure that Abreu specifically cited as protection against the freight rate spikes caused by the Red Sea and Hormuz disruptions. Executive Officer Leonardo Grimaldi added that this structure has allowed Suzano to keep supplying customers in conflict-affected regions, “surpassing eventual additional war-related surcharges to maintain continuity.”

The contrast with Finnish producers is instructive. The structural advantage that Nordic mills once held — proximity to European customers, established logistics, high-quality long-fiber pulp — has been partially offset by the energy cost premium that Russia’s war bequeathed to the continent. Latin American producers, further from the conflict zones and with lower production costs, have picked up some of that share.

For Nordic mills, the competitive picture is more complicated today than it was five years ago, and the gap will take longer to close than the market currently assumes. The wider softwood market is under acute stress. Leonardo Grimaldi described the softwood scenario as “unsustainable” during the Suzano’s Q1 2026 earnings call, with roughly 11 million tonnes of softwood capacity — around 40 percent of the global total — operating at a loss, pointing toward further consolidation and capacity reductions in the Northern Hemisphere. That trajectory is already visible: Domtar permanently closed its Crofton, BC mill in late 2025, removing 380,000 tonnes of NBSK capacity from the market.

Canadian producer Canfor reported a Q1 2026 operating loss of $73 million, with NBSK pulp list prices to China at $685 per tonne, down 14 percent year-on-year, and global producer inventories holding at 47 days of supply— the upper end of the balanced range. The company specifically cited the Iran conflict as a contributor to higher freight costs and pressure on global trade flows, and flagged petroleum-based supply chain constraints as an emerging drag on housing construction demand.

By late March, the strain showed up in pricing dynamics. Producers had conceded modest price reductions on softwood pulp, and an announced April price increase for bleached hardwood kraft was scaled back. The spread between northern bleached softwood kraft and bleached eucalyptus had narrowed to below $100 per tonne — its lowest level since mid-2024 and well below the cost premium of producing softwood. With Chinese demand weakened by domestic capacity expansion and stagnant downstream prices, the only viable strategy left to producers was to push higher costs into North American and European markets, where paper and board prices retain more pass-through capacity.

The Spanish producer ENCE offers a sharper illustration of where the pressure landed — and of how quickly the picture can shift. The company posted a €55 million loss for full-year 2025 as benchmark pulp prices averaged $1,086 per tonne, well below profitable levels, and cut roughly 15 percent of its pulp workforce as a result. By Q1 2026, losses had narrowed to €17.6 million — still negative, but half the level of the previous quarter — as the company advanced its restructuring and pulp prices began recovering. ENCE has announced a new benchmark price of $1,430 per tonne effective May 2026, a 32 percent increase from the 2025 average. Notably, its Q1 2026 report frames the Middle East conflict not only as a cost risk but as a commercial opportunity: disruptions to logistics routes from Asia and Latin America, it noted, are creating pricing power for European producers with local supply and energy self- sufficiency — exactly the position ENCE is working to occupy.

Portugal’s The Navigator Company reported full-year 2025 EBITDA of €376 million, down from €547 million in 2024 — a 31 percent decline that the company linked to a year “marked by economic and geopolitical instability,” alongside increased energy costs and tariff pressure. Its tissue and packaging segments, accounting for 32 percent of group EBITDA, provided a partial cushion, but were not enough to offset the pressure from falling pulp and paper prices. The pattern held across the sector: diversified product portfolios cushioned the blow, but did not eliminate it.

The supply chain vulnerability for European hygiene producers runs deeper than energy and polymers alone. According to data cited by EDANA, the United States accounts for more than 80 percent of global fluff pulp production capacity, and less than half of European demand can currently be met through non-US sources. Around 90 percent of fluff pulp consumed globally goes into absorbent hygiene products — diapers, adult incontinence, and femcare. For European manufacturers, that concentration of supply in a single geography — now subject to transatlantic trade friction on top of energy and raw material cost pressure — has moved from background risk to active concern. The market is still expected to grow; the debate is about who captures value along the way.

The investments being made now — Suzano’s new Ribas do Rio Pardo capacity, the long-term vessel contracts and oil hedging program used to insulate margins, the cost-reduction and transformation programs underway at producers from Magnera to Metsä Board to Ence- suggest that at least some producers may be treating the shift as structural.

The pulp value chain itself is being reshaped. Suzano has been approaching integrated pulp and paper producers in Western markets, encouraging them to transition away from in-house pulp production toward market purchases — what it calls its ‘de-verticalization’ agenda. The company said on its Q1 2026 call that it was close to confirming the first such agreement. A separate, more visible shift came with the $3.4 billion joint venture announced in June 2025, through which Suzano will acquire a 51 percent stake in Kimberly-Clark’s international tissue operations — a move that pushes the company further downstream into finished products.

WHAT COMES NEXT — AND WHAT NOBODY KNOWS

Nobody has a clean read on where this goes. The pace and outcome of the Gulf conflict, the trajectory of oil prices, the fate of the Suez Canal corridor, the durability of tariff regimes — all remains open.

The OECD’s mid-March 2026 Interim Economic Outlook, titled “Testing Resilience,” captured the trade-off facing the global economy: even with the conflict’s energy shock, baseline global GDP growth was projected to hold at 2.9 percent in 2026 — but G20 inflation was revised 1.2 percentage points higher to 4.0 percent, with energy prices assumed to be roughly 40 percent above pre-conflict levels for oil and 60 percent above for natural gas. The OECD’s downside scenario, in which energy prices stay around a quarter above the baseline alongside tighter financial conditions, would add a further 0.7 to 0.9 percentage points to inflation and reduce global GDP by around half a percentage point by year two.

By April, the IMF’s World Economic Outlook had downgraded its 2026 global growth forecast from a pre- conflict 3.4 percent to 3.1 percent under a limited-conflict reference scenario, with a severe scenario seeing growth fall to 2 percent in both 2026 and 2027. The range of outcomes is wide, and the industry needs to plan for more than one.

The risk table below summarizes the key pressure points as they currently stand.

|

RISK FACTOR

|

SEGMENT MOST AFFECTED

|

SEVERITY

|

LIKELY DURATION

|

|

Oil price above $100/barrel

|

Nonwovens, packaging, logistics

|

HIGH

|

12–24 months post-conflict

|

|

Red Sea / Suez Canal disruption

|

Pulp trade, tissue supply chains

|

HIGH

|

Structural; routing reorganization may persist beyond 2026

|

|

European energy cost premium

|

All paper grades, tissue

|

MEDIUM

|

Structural, multi-year

|

|

Polypropylene / polyester volatility

|

Nonwovens

|

HIGH

|

Linked to oil price path

|

|

Russian pulp supply loss to Europe

|

Tissue, specialty papers

|

MEDIUM

|

Largely absorbed; residual cost premium persists

|

|

LNG price spike (Qatar damage)

|

European mills, energy-intensive grades

|

MEDIUM

|

3–5 years for Qatar repairs

|

|

Inflation persistence from energy shock

|

All segments (cost-side)

|

MEDIUM

|

12–24 months elevated

|

|

US tariff disruption to pulp flows

|

Pulp, paperboard, containerboard

|

MEDIUM

|

Policy-dependent

|

On the more optimistic side, oil prices have historically retreated after conflict-driven spikes, often within 12 to 18 months of a ceasefire or resolution. Analysts suggest Brent could return to the $80–$90 range once Gulf infrastructure damage is assessed and supply begins recovering.

European energy markets, while still elevated, are better supplied than in 2022 — LNG import capacity has expanded, storage levels have generally been adequate, and the structural shock of the Russian gas cutoff has at least been absorbed, if not forgotten.

What the past three years have demonstrated, fairly clearly, is that the industry’s exposure to geopolitical risk is broader and faster-acting than many assumed. Energy prices, shipping costs, fiber supply, polymer prices, currency movements — all have been affected, sometimes simultaneously. Companies that invested in hedging, supply diversification, or vertical integration have generally been better positioned than those that did not. That observation may seem obvious in retrospect. It tends to be less obvious before the disruption arrives.

None of which means the next disruption will arrive the same form. It rarely does. What this industry can reasonably expect is more of the same underlying condition: a global supply chain that is tighter, more politically exposed, and less forgiving of thin margins than it was a decade ago. Planning around that reality is not pessimism. It is, at this point, just good practice.